Blogs & Articles: Nine Bitcoin Charts Already at All-Time Highs 🔗 3 years ago

- Category: Blogs & Articles | Nic Carter on Medium

- Author(s): Nic Carter

- Published: 17th November 2020 13:47

Why this bull run is fundamentally different from 2017

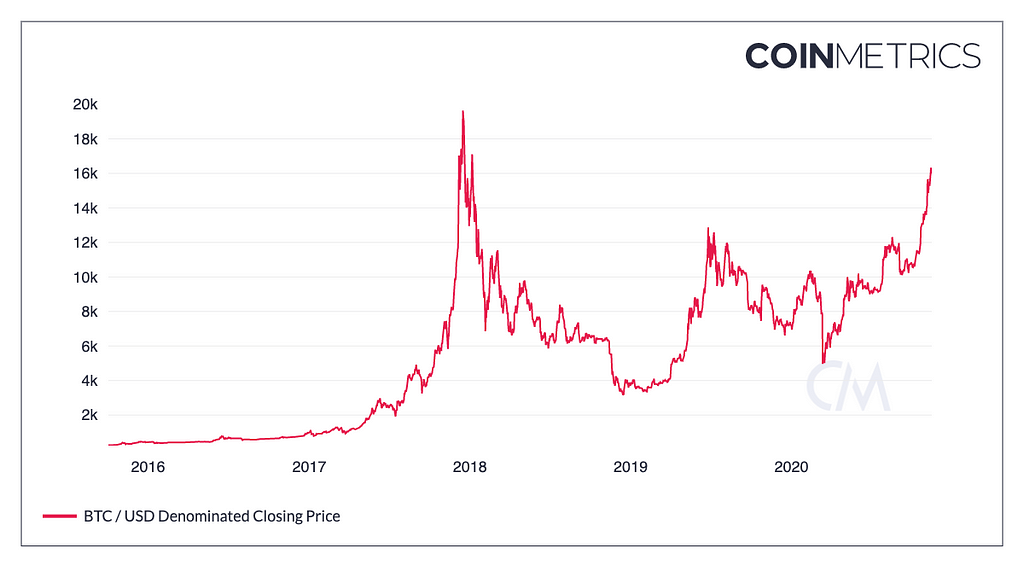

Bitcoin is nearing its prior all-time high (ATH), set in December 2017. It’s entirely plausible that we could regain the heady $20,000 level within the next few weeks or months.

This time, it’s happening without much fanfare, and without the Initial Coin Offering (ICO) phenomenon which intensified the price action (investors bought BTC in order to participate in ICOs, driving the price up).

If you gauge metrics of retail investor interest in the asset, whether it’s tweets or google searches, Bitcoin is still languishing well below it’s highs. This is causing a fair amount of puzzlement.

Many are wondering what the cause of Bitcoin’s renewed energy is. I figured I would present a few Bitcoin-related charts that are already hitting new all-time highs, in order to clarify the phenomenon a bit.

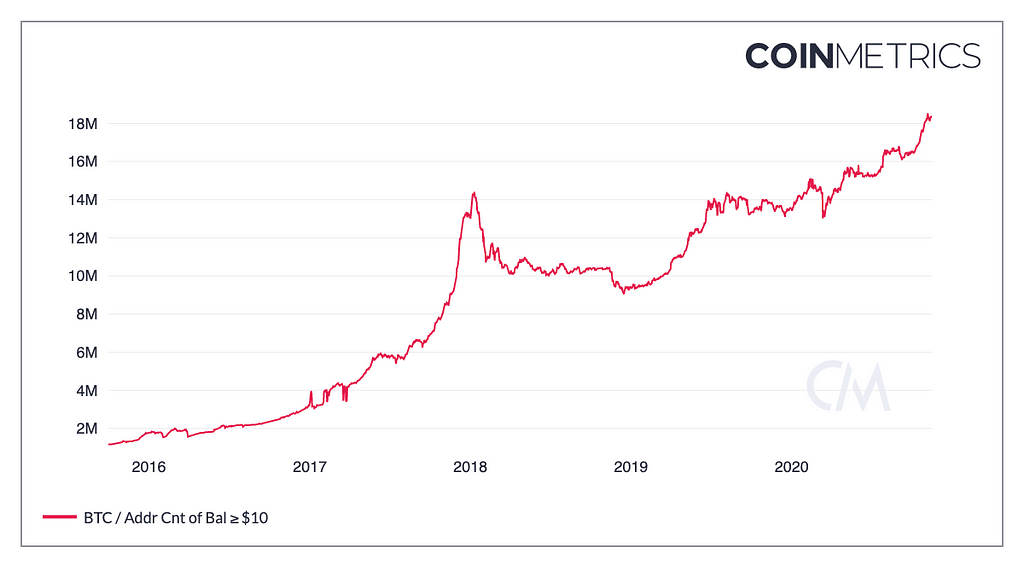

Addresses with a balance of $10 or more

This first chart proxies a fundamental driver of Bitcoin’s price, adoption. Quite simply, more people own Bitcoin today than did in 2017 — by a fair amount.

Source: Coin Metrics

Source: Coin Metrics

This chart shows the number of addresses on the Bitcoin ledger owning $10 or more worth of the asset. It’s well above its late 2017 level. This shows the supply of Bitcoin getting more and more dispersed, especially into lot sizes that are consistent with retail investors. The chart looks much the same — at all-time highs— for other thresholds, whether $1, $100, or $1,000. At all of these levels, there are simply more addresses on the ledger holding Bitcoin.

Of course, one address on-chain does not necessarily correspond to one person. Large exchanges custody Bitcoin in omnibus accounts on behalf of many users, and regular users can control many addresses, so there’s error in both directions. But as long as the relationship between humans and the number of addresses on-chain that represent them is somewhat consistent, this is a useful directional metric to assess user growth.

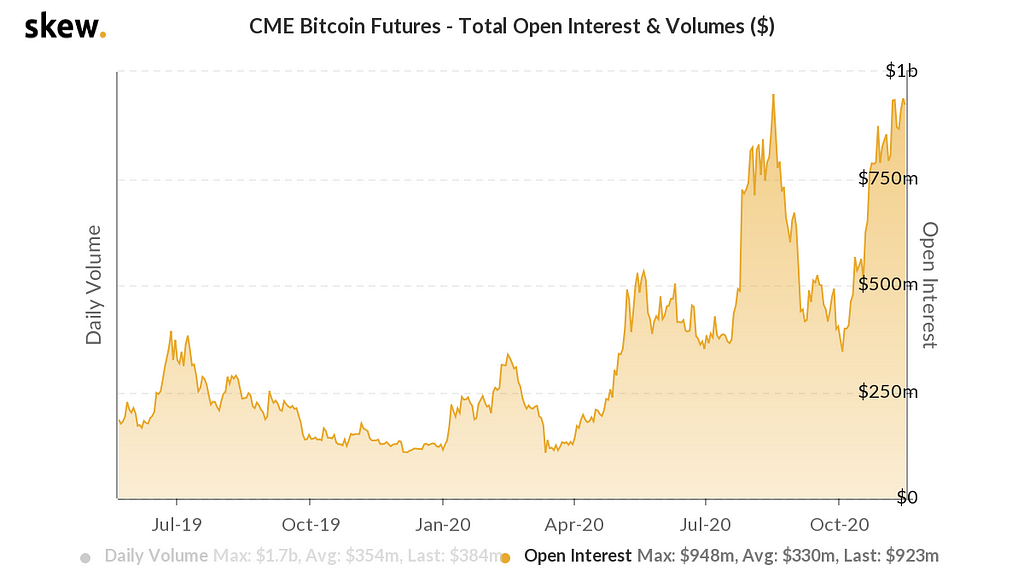

Open Interest on the CME Bitcoin Futures

The open interest in futures refers to the total value of outstanding contracts that have yet to be settled. The CME Bitcoin Futures product is notable because it’s a liquid Bitcoin product at the world’s largest derivatives exchange, which investors of all stripes have access to. Unlike a lot of Bitcoin exchanges, the CME is plugged into established clearing infrastructure — effectively the plumbing capable of moving trillions of dollars around.

Indeed, when Renaissance Technologies, one of the world’s most lucrative hedge funds, announced that they would include Bitcoin in their universe of tradeable assets, their instrument of choice was the CME cash-settled Bitcoin futures product. The CME is a natural choice for many large and highly-regulated allocators, because they don’t want to deal with the operational complexities that involve taking custody of Bitcoin, they may already actively trade on the exchange, and their regulators are most likely already comfortable with it. No need to evaluate the risk of a brand new platform.

Source: Skew

Source: Skew

This product originally launched on December 17, 2017, the precise top of the last bull run for Bitcoin. The chart doesn’t include data prior to mid 2019, but if you look at historical coverage of the CME’s Bitcoin product, you can see that open interest is indeed at ATHs (well, it’s a smidge below it’s ATH set in August 2020).

The other important thing to note is that the CME is a highly-regulated U.S. domiciled exchange under the aegis of the Commodity Futures Trading Commission. Unlike certain offshore Bitcoin exchanges, it has a robust trade surveillance framework and is considered to be extremely reliable. This does not make the venue immune to market manipulation, but it does mean that manipulators can be caught. This matters for Bitcoin, because a lack of surveilled and orderly markets to trade the asset is the chief reason the Securities and Investment Commission rejected a Bitcoin ETF in the past. As certain offshore exchanges face enforcement actions and are marginalized, the growth of onshore, orderly markets that regulators are very comfortable with, means that the prospects for a Bitcoin ETF are much sunnier.

Put simply, a Bitcoin ETF would be an enormous catalyst for the asset. The existence of a Bitcoin ETF would enable entire categories of market participants to get efficient and convenient access to the asset, who simply weren’t able to get exposure to it before.

The industry has been holding its breath waiting for an ETF for the past half decade. I vividly remember being disappointed at the SEC denial of the Winklevoss $COIN Bitcoin ETF in March 2017. We’ve come a long way since then; market structure is such that new ETF applications would be extremely credible, with the increasing prominence of onshore markets like the CME being of paramount importance.

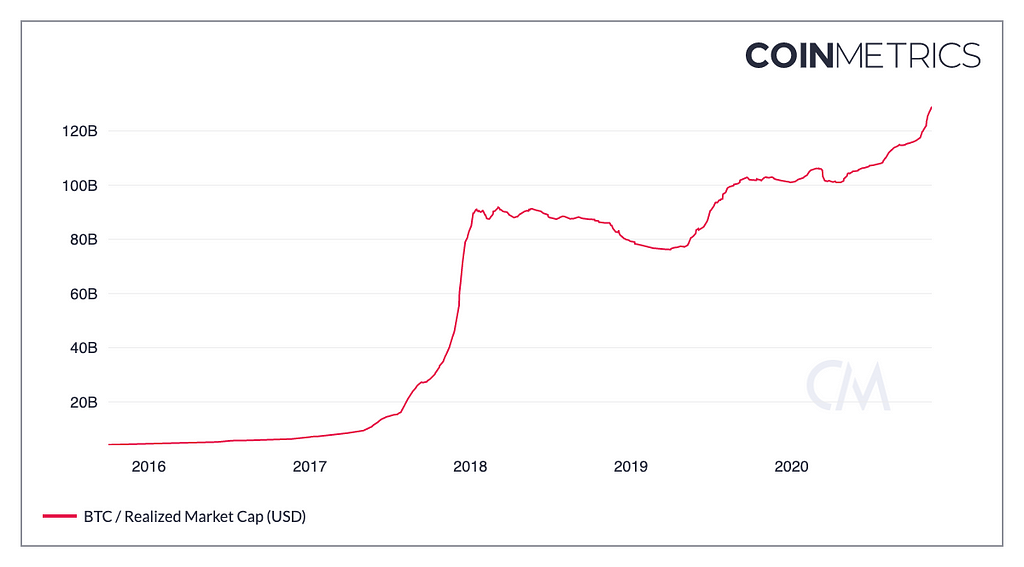

Realized Capitalization

Realized Capitalization is an alternative to Market Capitalization, designed to take into account the reality of when Bitcoins changed hands. Instead of pricing every outstanding unit of Bitcoin at the last market price, it prices every unit of Bitcoin according to when they last moved on-chain. This is possible to ascertain because Bitcoin’s ledger is transparent, and we can account for every single coin.

This takes into account the liquid supply of Bitcoin in a practical sense. Realized cap ignores the market value of Bitcoins that haven’t moved since 2009 (when Bitcoin did not have a market value). You can think of it as roughly measuring the aggregate cost basis of all the current Bitcoin holders.

Source: Coin Metrics

Source: Coin Metrics

Realized cap sits at $129B today, well above its $90B peak in early 2018. What this tells us is that Bitcoin is substantially more liquid at these levels, with investors less eager to sell. In late 2017/early 2018, the unit price was higher (the Coin Metrics reference rate lists the highest 00:00 UTC daily close at $19,640 on Dec. 16, 2017), but less of the supply had changed hands at those rarefied levels. This also explains why the price collapsed so quickly from there. It simply couldn’t be sustained, as investors in the aggregate had a cost basis far below that threshold, and were eager to take profit. The 2017 bull run was more of a melt-up, driven by ICOs, press coverage, and retail investor excitement. This bull run is more of a sustainable slow burn.

Today, the picture looks very different. The supply has significantly churned and a lot of early investors have cashed out, giving way to new blood. These investors, who bought their coins in the last couple years, are presumably not as eager to lock in a profit at $20k as someone who had been holding Bitcoin since it was $1. Thus, a higher realized cap is an indication of greater maturity and capacity for patience in the current investor set.

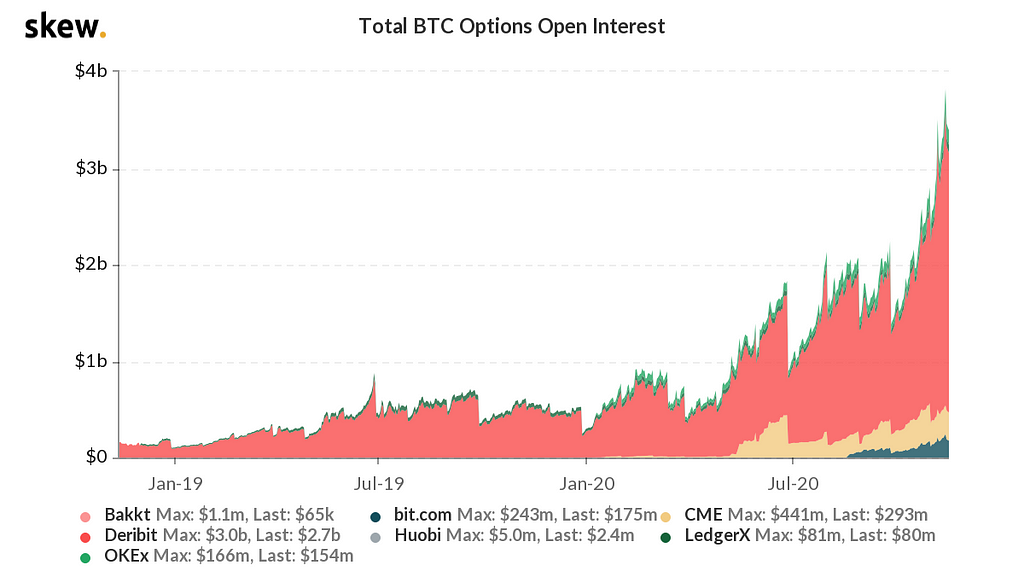

Bitcoin Options Open Interest

Open interest in an options contract adds up the value of the outstanding, un-exercised options. (Options traders will grumble at this methodology, because it can be skewed by options trading at silly strike prices like $32k.) While in absolute terms, the numbers are still fairly low, the incipient but maturing options market tells us a thing or two about Bitcoin today.

Source: Skew

Source: Skew

Just like derivatives first came into existence for farmers to hedge their exposure to crops and lock in a specific price for their harvest (and get liquidity on their future crops so they could buy seeds and fertilizer today), so too are options useful for the producers of Bitcoin — the miners. Miners can tell, roughly speaking, how many Bitcoins they will mine based on their equipment, under reasonable assumptions about hashrate. If they want to get an ‘advance’ on the coins they expect to mine, they can sell calls. This means they promise to deliver coins at a certain price on a certain date — but they get paid for that promise today. And with that cash advance, they can go ahead and finance their operation more efficiently.

What this chart tells me is that the producers of Bitcoin now have access to more sophisticated financial products which they can use to hedge their exposure. In theory, this should mean that the mining industry is more stable and less exposed to boom and bust periods. It lets miners focus on running their operations efficiently, and frees them from the burden of worrying about their unhedged exposure to their equipment.

Additionally, the growth of options means that traders, who take the other side of those bets, have more creative ways to express their view on Bitcoin. For instance, using these instruments, it’s now viable to bet not on Bitcoin going up or down, but on an expectation of future volatility (or a lack thereof). These instruments simply didn’t exist in 2017. Fundamentally, by giving sophisticated investors more tools, Bitcoin can accommodate more capital inflows.

Bitcoin priced in Turkish Lira

Investors often track Bitcoin’s performance in dollar terms, but the truth is that much of the world’s population denominates the performance of financial assets in their local currency. After all, they may not have access to the dollar-based banking system. The further away you are from NY, and the more hops correspondent banks have to take to get to your local banks, the more expensive your access to the dollar is. U.S. banks aren’t fond of doing business with individuals overseas. They are risky to service, and risk makes things expensive. Thus, these U.S. banks have a tendency to “derisk” their exposure to non-U.S. clients.

Billions of savers worldwide must therefore reckon with inflationary currencies, or monetary repression — a state of affairs where they don’t have the freedom to move their assets around. This latter phenomenon is often imposed by central banks that fear currency flight and accompanying depreciation. It comes at the cost of self-determination on the part of savers.

While most people reading this will have the luxury of saving in dollars or euros, it’s important to remember that inflationary currencies are the reality for a significant share of the world’s population. We measure the Bitcoin in dollar terms, but the dollar is among the least inflationary of all global currencies. Because Bitcoin is such a great non-sovereign wealth store, being highly portable, concealable, and seizure-resistant, when sovereign currencies start to fail, it looks attractive. Bitcoin exchanges in Turkey have received a huge boost this year as the Lira has endured a long slide. In absolute terms, Turkey is the 12th-most popular country for exchange web visits.

BTCTRY, Tradingview (retrieved from CoinGecko)

BTCTRY, Tradingview (retrieved from CoinGecko)

The Bitcoin chart in Turkish Lira terms looks similar in shape to the BTCUSD chart, except the denominator keeps depreciating, causing it to explode to new ATHs in 2020.

The Lira isn’t the only sovereign currency in which Bitcoin is already trading well beyond its prior highs. Other currencies where Bitcoin has already hit new highs since 2017 include the Argentine peso, the Russian ruble, the Venezuelan bolivar, the Brazilian real, the Colombian peso, the Lebanese pound, the Sudanese pound, and several others. Those countries alone account for 523 million people.

The distribution of enthusiasm for Bitcoin exchanges globally is revealing. Other countries topping rankings for crypto adoption include those burdened by onerous capital controls (China, Ukraine) or highly inflationary or unstable currencies (Venezuela, Nigeria, Colombia, Argentina). These are real catalysts driving everyday savers to desert their local currencies for Bitcoin, stablecoins, and other cryptocurrencies.

Three years ago, Bitcoin exchange infrastructure fundamentally wasn’t as well developed, nor were there as many individuals worldwide with accounts on exchanges. Those points of liquidity where savers could exit fiat and move to cryptoassets have developed significantly over the last three years since the last bull run. The data bears this out: the 2nd Cambridge Cryptoasset Benchmarking Study, published in Dec. 2018, found 35 million identity-verified cryptoasset users at exchanges worldwide, while the 3rd study in the series, published Sep. 2020, found 101 million identity-verified accounts. Quite simply, exchange infrastructure has matured and proliferated to the point that exiting local fiat for digital assets is a viable proposition for a meaningful share of the world’s population.

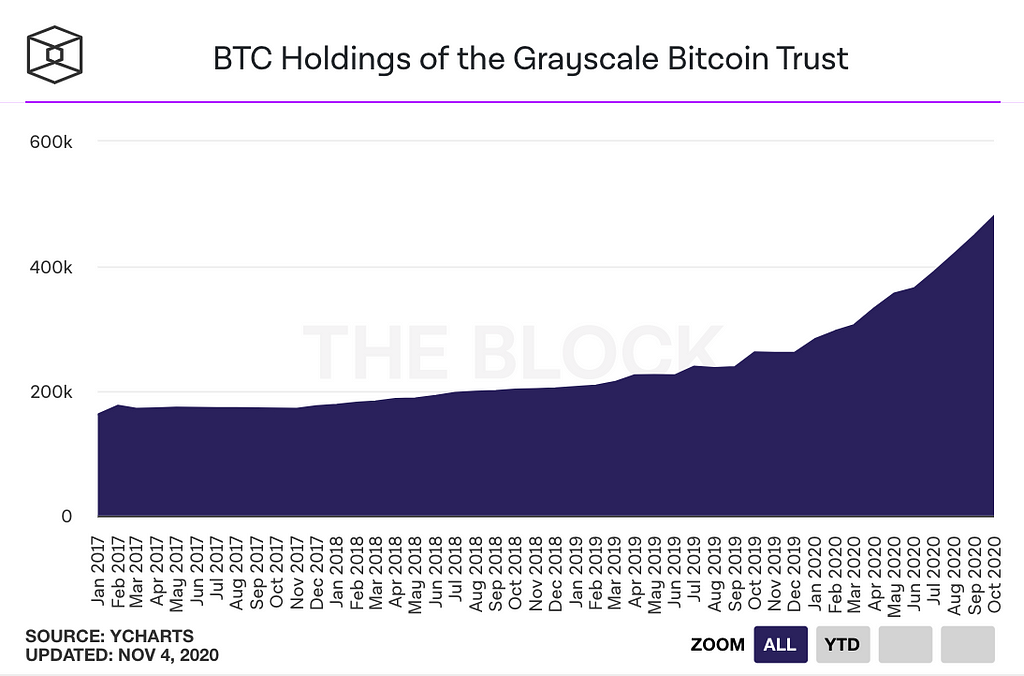

Bitcoin held by Grayscale

One critical chart bearing out the enthusiasm for Bitcoin is the number of units held by the asset manager Grayscale. At the time of writing, this topped 500k BTC, making GBTC the single most popular financialized version of Bitcoin.

Source: The Block

Source: The Block

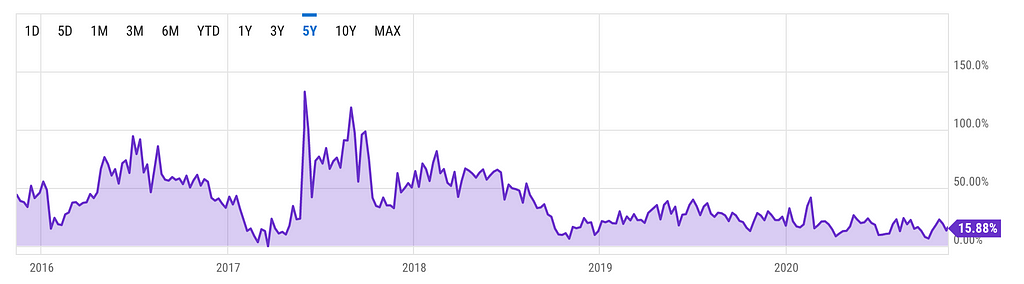

Because the GBTC is a trust product trading on the OTCQX marketplace, and newly-created shares take six months to mature, there is typically a mismatch between the market value and the net asset value (NAV) of shares. This difference is expressed as a premium. As of today, the premium stands at 15.8%, meaning that if you deployed $100 into GBTC, you would only be receiving $84.2 worth of exposure to Bitcoin.

Source: Ycharts

Source: Ycharts

A number of trading firms borrow Bitcoin, create new units of GBTC at NAV, wait six months for them to mature, and then liquidate them at market price, pocketing the premium (minus the interest on the loan). Despite this continual slow-motion arbitrage, the premium has lingered for virtually the entire history of GBTC. The lingering premium to NAV is evidence for a continual enthusiasm for the product among investors. GBTC is popular because it is available on mainstream brokerages like Fidelity and Schwab and can be held in a tax-advantaged way, in an IRA or 401k.

The immense growth of GBTC in 2020 is evidence that there is a class of allocators who are content to obtain inefficient exposure to Bitcoin. Buyers of GBTC are not your typical techie crypto investors, who are more likely to make an account with one of the crypto exchanges and take ownership of spot Bitcoin (and avoid a costly premium). The continued growth of GBTC is evidence that an older and less crypto-native cohort of investors retains a significant appetite for the asset, even if the exposure is inefficient.

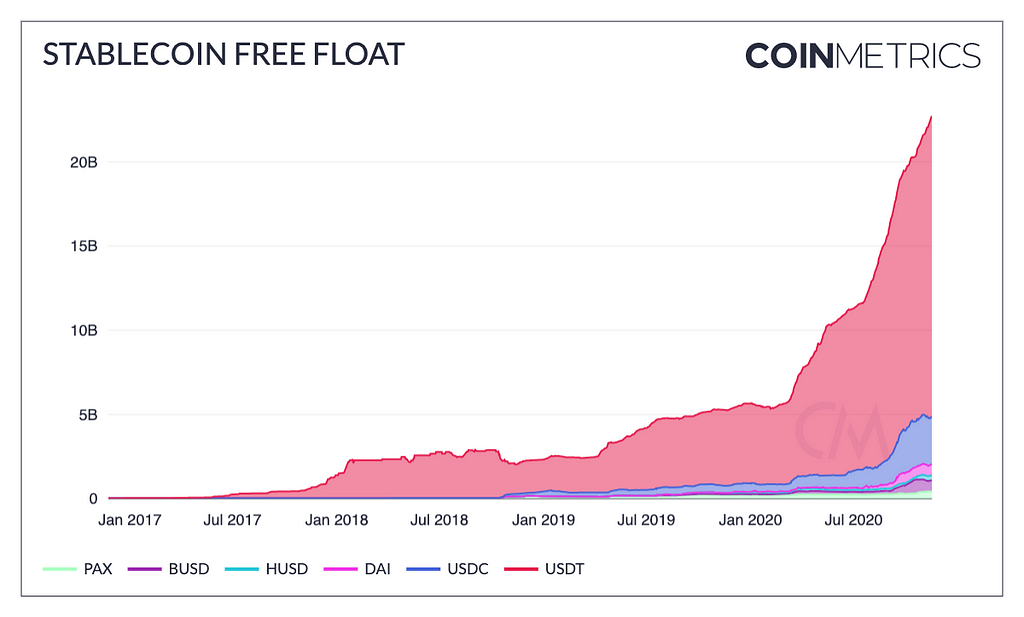

Stablecoin free float

Now many of you will be reading critical takes on Bitcoin’s current rally from people insistent that stablecoins like Tether are somehow responsible for its price. I would invite you to ask these critics if they are active participants in crypto markets. If not, you can safely disregard their opinions. It is only individuals with experience creating and redeeming stablecoins, and experience allocating capital in the cryptoasset space, that should be considered credible sources on this issue. Otherwise it is quite simply too difficult to understand the dynamics at play.

And indeed, much of this critical analysis relies on a since-debunked paper by Griffin and Shams that relies on a narrow sample period and questionable methodology to allege a relationship between the issuance of Tether and the BTC unit price in 2017. More recent scholarship, including Viswanath-Natraj and Lyons, using a broader sample period, has found no causal leading relationship between Tether issuance and the Bitcoin price. Additional work from Wang Chun Wei confirms the lack of a correlation between Tether creation and Bitcoin returns.

And empirical reality bears this out too: from February 2018 to July 2019, Bitcoin was effectively flat (it started and ended the period at $11k), while the supply of stablecoins increased from $2.3B to $11.5B. If the creation of stablecoins somehow buoyed the price of Bitcoin, why was its price unchanged as the supply of stablecoins increased by 400 percent? The critics fixated on Tether have no answer for this question.

The truth is that the creation of Tether and other stablecoins (the supply of non-Tether stablecoins is over $5B today) should be understood not as purchases or capital inflows, but simply like-for-like asset swaps. Stablecoins are created when an entity with fiat on their balance sheet wants access to crypto-native liquidity. They merely exchange commercial bank dollars for a tokenized representation of the same. Firms that denominate their balance sheets in stablecoins or hold stablecoins as working capital include market makers, proprietary trading firms, exchanges, venture capital firms, and generally speaking any businesses operating in the crypto industry with crypto-denominated expenditures. After the panic in mid-March 2020, a number of firms transformed their balance sheets from commercial bank dollars to tokenized dollars circulating on public blockchains, so that they could be more nimble the next time an opportunity like that arose.

Despite this, the growth in stablecoins is positive for Bitcoin, not because of the conspiracies around unbacked issuance, but simply because it means that the liquidity environment is vastly improved.

At the previous Bitcoin ATH, only $1.5B worth of stablecoins existed. Today that number stands at $22.7B. Stablecoins have created a pool of stable-value liquidity which is not exposed to volatility. Interestingly, while many exchange venues have become “Tetherized” — as in, USDT is the main trading pair and settlement asset, displacing Bitcoin’s former role in this function, Bitcoin’s price remains robust. This is testament to Bitcoin’s evolution as a product, from a reserve asset for exchanges — exposed to trader willingness to trade long tail assets on exchanges — to an independent monetary asset in its own right, beloved of hedge fund managers and commodities traders.

The fact that Bitcoin has nearly completely recovered its prior highs in market cap while stablecoins have taken its mantle as reserve assets for the crypto industry suggests that it has taken on a life of its own

Lastly, capital existing in tokenized fiat format tends to enter the crypto industry but not leave. This is because crypto rails are fundamentally more convenient, more globalized, and less encumbered than traditional payment and settlement rails. Thus a material portion of the $22.7B worth of of tokenized USD circulating on public blockchains represents dry powder that could well be allocated to risk assets like Bitcoin. If there is a run on any of these stablecoins, or their backing comes into question, the natural direction to flee will be in the direction of censor-resistant assets like Bitcoin which can absorb that much liquidity at short notice. Presumably, if a stablecoin suspends convertibility, holders will not be able to conveniently exit at fiat off-ramps — but they will be able to flee into the blue chip cryptoassets, of which Bitcoin is by far the largest and the most liquid. Thus if stablecoins do face adverse outcomes, the result is most likely a significant capital inflow into Bitcoin.

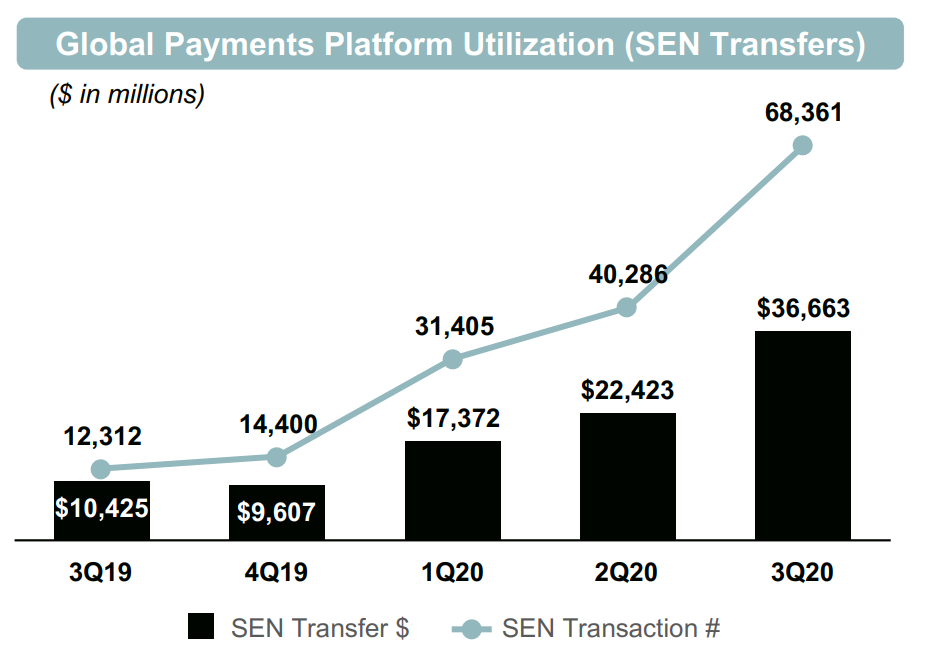

Silvergate’s Settlement Network

Another critical piece of financial market infrastructure which has been underappreciated has been banks like Silvergate which service the industry. In 2017, and even more so during the primordial era of the crypto industry, bank relationships were extremely hard to come by, and only the largest and most credible crypto corporations could acquire banking. Today, a number of banks in the US actively service crypto businesses: chiefly among them, Silvergate, Signature, and Metropolitan. Additionally, two new entities — Avanti Bank and Kraken Financial — have received charters under Wyoming’s Special Purpose Depository Institution legislation, meaning that they are eligible to get access to the Federal Reserve (while also managing cryptocurrency assets on behalf of clients).

Put simply, the bank environment, long a critical challenge for crypto businesses in the U.S., is vastly ameliorated today as compared with three years ago during the last bull run. By virtue of its publicly-traded status, Silvergate’s impressive traction is semi-transparent. One of their flagship products in their intra-bank settlement product, the Silvergate Exchange Network (SEN). The SEN enables clients of Silvergate to settle with each other Since they bank so many crypto businesses, transactions on the SEN are a proxy of sorts for the vibrancy of U.S. domiciled firms in the industry.

Source: Silvergate Q3 Earnings Presentation

Source: Silvergate Q3 Earnings Presentation

In the third quarter of 2020, the SEN processed $36B in transfers. These sorts of financial infrastructure products, while not typically understood as critical to Bitcoin, enable the efficient clearing and settlement of fiat funds between crypto firms in the U.S. This is yet another product that simply did not exist in 2017.

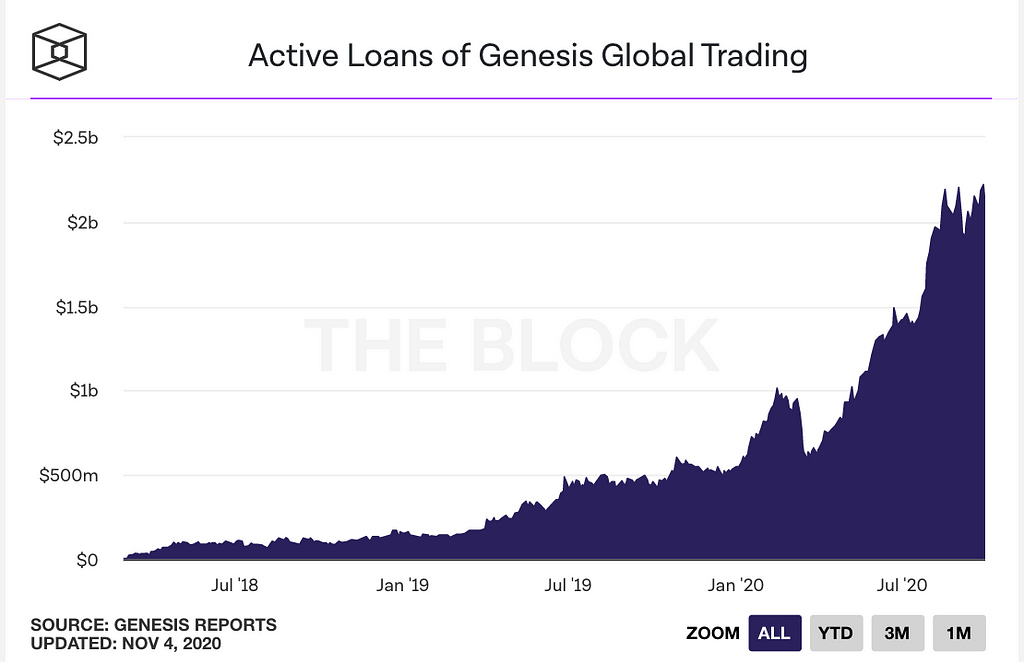

Growth of crypto-native credit

Another underappreciated story is the wide availability of crypto-native credit today. As with some of the other phenomena mentioned here, professional intermediation in the lending space simply didn’t exist in late 2017 — although certain p2p credit markets existed, for example on Bitfinex. What credit permits is capital efficiency for market makers, arbitrage firms, and hedge funds active in liquid markets. The fragmented liquidity environment in the crypto industry means that these firms must lock up liquidity on a number of exchanges simultaneously. This can make certain strategies very costly from a capital perspective, which is where credit providers like Genesis and BlockFi come in. The insertion of credit onto blockchains has the practical effect rendering spreads tighter and inter-exchange price dislocations less common. Additionally, any business with Bitcoin or stablecoin-denominated expenditures — like Bitcoin ATM companies — can benefit from the convenience of credit.

There are many charts to choose from to depict the growth of credit, but the outstanding loan portfolio of Genesis, the largest institutional-focused lender, is illuminating.

Source: The Block

Source: The Block

While some Bitcoiners are opposed to the insertion of credit into the industry, I am firmly of the opinion that abundant credit has dramatically ameliorated the liquidity environment and tightened spreads.

Conclusion

To sum up, today’s market is far more mature, more financialized, more surveilled, more orderly, more restrained, less reflexive, more capital-efficient, and more liquid than the market that powered the prior bull run in 2017. Positive catalysts like a Bitcoin ETF appear to be plausible in the not too distant future. The quiet and diligent work that entrepreneurs have done in the last three years, out of the public eye, has equipped the industry to handle far more

In these nine charts, I covered a variety of factors where clear improvements are manifestly present when we compare today’s market environment with the bull run of yesteryear.

I did not even mention the rise of true institutional-caliber custodians like Fidelity Digital Assets (launched in late 2018), a potent development in the history of the industry. Nor did I cover the rise of sophisticated order management services which facilitate the process of attaining exposure to large quantities of Bitcoin. And I did not cover sophisticated digital asset settlement networks like Fireblocks which rely on novel cryptography and derisk the process of making on-chain transactions. Nor did I mention the unbundling of exchange, brokerage, and custody functions, and the specialization of firms within each segment. And I did not mention the rise of institutional-caliber capital markets data firms creating credible data feeds and reference rates to power indexes and other financial products. The positive developments which we have witnessed in the last three years are too many to enumerate.

Ultimately, though, market infrastructure alone is insufficient to spark excitement around Bitcoin. It is solely the plumbing through which capital can flow to the asset. The true catalyst for Bitcoin this year has been the greatest monetary expansion we’ve witnessed in the modern era — an experiment that has our fiat system teetering on the edge of oblivion.

USD M1 Money Stock, y/y change. Source: FRED

USD M1 Money Stock, y/y change. Source: FRED

Perhaps more than any of the factors mentioned here, the growth in money supply is the fundamental catalyst for renewed interested in hard assets like Bitcoin, especially among more serious macro-focused allocators. This run is characterized by global macro hedge funds and commodities traders taking a second look at Bitcoin, rather than an explosion of interest from retail investors.

These are the macroeconomic tailwinds powering the resurgent interest in the industry. While the future of CPI inflation for the dollar is not clear, we look set for negative real interest rates for the foreseeable future. In light of this reality, it’s no surprise that zero-yielding assets like gold and Bitcoin have caught the attention of these allocators. This time, Bitcoin is ready.